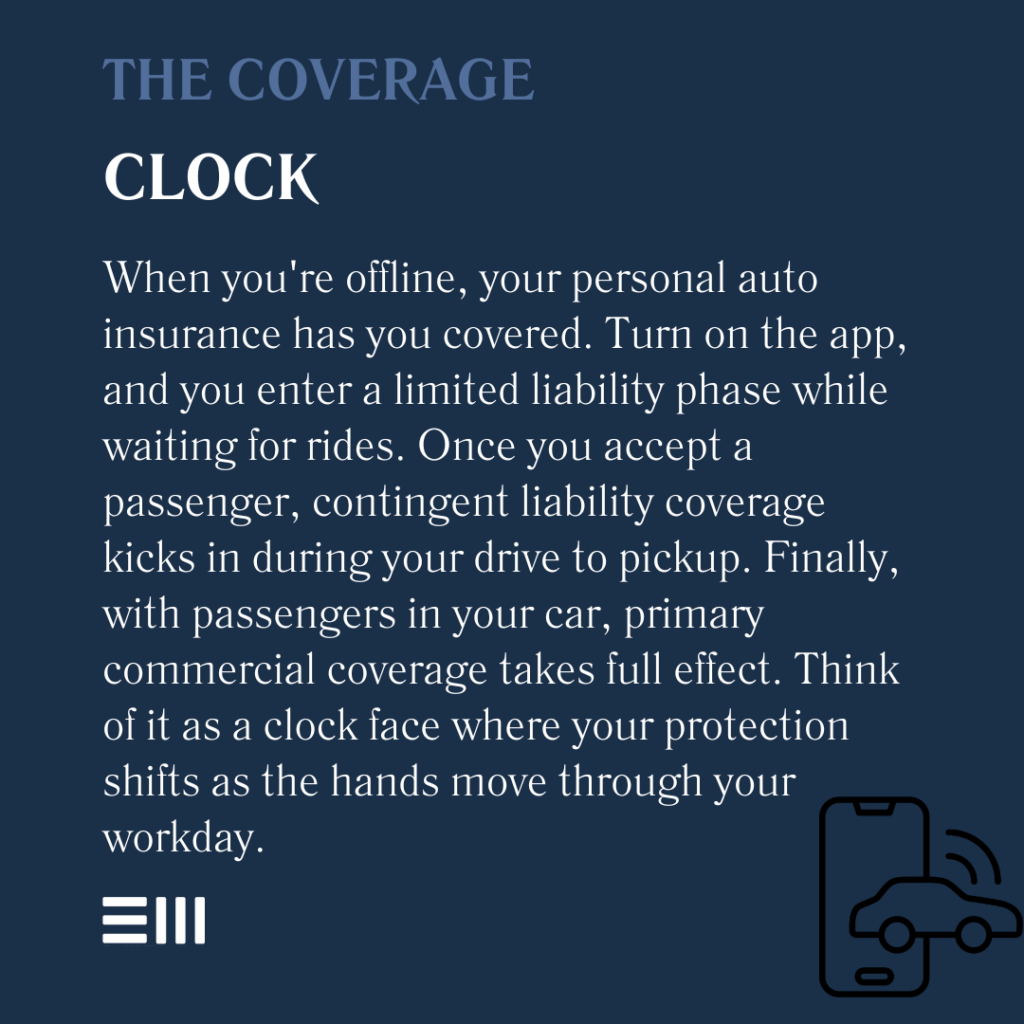

Have you ever wondered what happens if someone else drives your car and causes an accident? Or if you’re behind the wheel of a borrowed vehicle, who’s really responsible for the damage?

Understanding personal driver liability coverage is crucial to protecting yourself and your finances in these situations. This type of insurance coverage isn’t just about your car—it’s about you as a driver, wherever you are. You’ll discover what personal driver liability coverage means, why it matters, and how it can save you from unexpected costs.

Keep reading to make sure you’re fully covered and confident every time you get behind the wheel.

What Is Personal Driver Liability Coverage

Personal Driver Liability Coverage protects you if you cause damage or injury while driving. It covers costs like medical bills, repairs, and legal fees. This coverage is important when driving a car you do not own. It helps pay for damages if you cause an accident.

This coverage differs from regular car insurance because it follows the driver, not the car. If you borrow a friend’s car, your personal driver liability can provide protection. Without it, you might have to pay out of pocket for damages.

Coverage limits show the maximum amount your insurer will pay. Higher limits mean better protection but can cost more. Always check what your policy covers before driving someone else’s vehicle.

Why Liability Coverage Matters

Liability coverage protects your money if you cause an accident. It helps pay for damages and injuries to others. Without it, you may have to pay a lot out of pocket.

You have a legal duty to carry liability coverage. Driving without it can lead to fines or losing your license. This coverage shows you are responsible and follow the law.

| Coverage Limit | What It Means |

|---|---|

| Bodily Injury per Person | Maximum paid for one person’s injury |

| Bodily Injury per Accident | Total amount paid for all injured in one accident |

| Property Damage | Max paid for damage to others’ property |

Choosing correct limits is key. Too low means you might pay leftover bills. Too high increases your premium but offers better protection.

Who Is Covered Under This Policy

Authorized drivers are people allowed by the policyholder to drive the car. These drivers have coverage under the personal driver liability policy. This means if they cause an accident, the insurance may pay for damages.

Permissive use situations happen when someone not listed on the policy borrows the car with permission. Most policies cover these drivers for liability, but coverage limits may be lower. Always check your policy details.

Non-owner drivers don’t own a car but drive others’ vehicles. They need special insurance called non-owner liability coverage. This protects them if they cause an accident while driving a borrowed or rented car. It covers bodily injury and property damage.

Differences Between Car And Driver Coverage

Insurance following the driver means the coverage moves with the person. This type of insurance protects the driver no matter which car they drive. It is useful for people who often borrow or rent cars. It covers liability if the driver causes an accident. Non-owner car insurance is an example of this type. It does not cover the car but protects the driver.

Insurance following the vehicle stays with the car, not the driver. The coverage applies to whoever drives the car with permission. If a friend borrows the car, they are covered under the car’s insurance. This is called “permissive use.” It protects the car owner from liability when others drive their car.

Non-owner Car Insurance Basics

Non-owner car insurance is for people who drive cars they do not own. It provides liability coverage if you cause an accident while driving someone else’s car. This insurance helps pay for damage to others and their property.

It includes:

- Liability protection for injuries or damage you cause.

- Coverage if the other driver has no or too little insurance.

- Sometimes medical payments for injuries to you or others.

In Texas, this insurance works by covering you, not the car. It is useful if you often rent, borrow, or drive different cars. Your own car insurance usually won’t cover you in these cases.

Consider non-owner insurance if you:

- Drive cars you do not own regularly.

- Do not own a car but still drive.

- Want protection beyond what rental companies offer.

Common Scenarios And Liability Risks

Friend or Family Driving Your Car: Your insurance usually covers friends or family driving with permission. But, coverage limits and rules vary by policy. If they cause an accident, your liability coverage pays for damage or injury.

Rented or Borrowed Vehicles: Personal driver liability coverage may not apply to rented cars. Rental companies often require their own insurance or coverage through a credit card. Borrowed cars might be covered, but check the owner’s insurance first.

Uninsured or Underinsured Motorists: This coverage protects you if another driver causes an accident but lacks enough insurance. It helps pay for your injuries and damages. Without it, you might have to pay costs yourself.

Tips To Maximize Your Liability Protection

Choosing adequate coverage limits ensures you have enough protection for damages. Low limits can leave you paying out of pocket. Higher limits cost more but offer better security. Balance your budget with your risk level.

Adding riders or endorsements can extend your coverage. Common options include uninsured motorist protection and roadside assistance. These extras fill gaps standard policies may miss. Check what fits your needs best.

Regular policy reviews keep your coverage up to date. Life changes like moving or buying a new car affect your needs. Review your policy yearly to adjust coverage limits or add endorsements. Staying current avoids surprises during claims.

How To File A Liability Claim

After an accident, gather all important information. This includes names, phone numbers, and insurance details of all drivers involved. Take photos of the damage and the accident scene. Write down the time, date, and location of the accident.

Contact your insurer as soon as possible. Provide them with the accident details. Be honest and clear when answering questions. Keep a record of all communications with your insurance company, including names of representatives you speak with.

Follow the insurer’s instructions carefully. They may ask you to fill out claim forms or provide additional documents. Cooperate fully to speed up the claim process. Stay calm and patient during this time.

Liability Coverage Costs And Discounts

Premiums for personal driver liability coverage depend on many factors. Age, driving record, and car type all matter. Younger drivers or those with accidents pay more. The car’s value and safety features also affect costs.

Many insurance companies offer discounts to lower premiums. Safe driver discounts reward good records. Multi-policy discounts apply if you bundle insurance. Some offer discounts for low mileage or defensive driving courses.

Balancing cost and coverage is key. Cheaper premiums may mean less protection. Higher coverage limits cost more but protect better. Choosing the right mix depends on your budget and needs. Always check what each policy covers before buying.

Liability Laws In Austin, Texas

Texas law requires all drivers to carry minimum liability coverage. This covers injuries or damage to others if you cause an accident. The state minimum limits are $30,000 for injury per person, $60,000 per accident, and $25,000 for property damage. Austin may have additional rules or enforcement practices to ensure drivers comply with these laws.

Local regulations in Austin emphasize strict adherence to liability laws to protect all road users. Insurance companies consider these rules when setting coverage options and premiums. Drivers must understand how city rules affect their liability coverage needs.

Liability coverage in Austin often reflects both state and local laws. Coverage impacts your financial protection if you cause a crash. Higher coverage limits offer better protection but might cost more. Knowing local laws helps choose the right coverage for safe driving.

Frequently Asked Questions

Is Personal Liability Coverage Worth It?

Personal liability coverage protects you from financial loss if you cause injury or damage. It offers valuable peace of mind.

Is My Girlfriend Covered If She Drives My Car?

Your girlfriend is usually covered under your car insurance if she has your permission to drive. Coverage depends on your policy terms.

How Much Does $100,000 Of Personal Liability Insurance Cost?

$100,000 of personal liability insurance typically costs between $100 and $300 annually. Prices vary by location and provider.

What Happens If My Friend Drives My Car And Gets Pulled Over?

If your friend drives your car and gets pulled over, your insurance typically covers liability. Your friend must have permission to drive. Your friend may face tickets or penalties. Your insurance may affect your premiums if your friend causes damage or violations.

Conclusion

Personal driver liability coverage protects you from financial loss if you cause an accident. It covers damages and injuries to others while you drive. This coverage is important for anyone who often borrows or rents cars. It helps avoid costly bills and legal troubles.

Always check your insurance policy to understand your protection limits. Staying informed keeps you safe on the road. Consider adding personal driver liability coverage for peace of mind. Drive responsibly and protect yourself from unexpected expenses.

Read More

- Dui Lawyer Free Consultation: Expert Help Without Cost Today

- Convicted Driver Insurance Coverage: Essential Tips for Affordable Protection

- Cheap Driver Insurance Online: Save Big with Top Deals Today

- Driver Insurance Quote Comparison: Find the Best Rates Fast

- Traffic Ticket Attorney Cost: What You Need to Know Now

- Reckless Driving Lawyer near Me: Expert Help to Win Your Case

- License Suspension Legal Help: Expert Tips to Regain Your Drive

- Young Driver Insurance Rates: How to Slash Your Premiums Fast

- High Risk Driver Insurance Quotes: Save Big with Expert Tips

- Auto Refinance Quote Calculator: Save Big with Easy Savings Today